우수 논문 발표 세미나 개최 : Geodesic flow kernels for semi-supervised learning on mixed variable tabular dataset

2025.01.13- Date

- 2025-01-14 15:00:00

- Lecturer

- 황윤태

- Venue

- Online(Zoom)

📅 세미나 정보

📅 세미나 정보🔸일시 : 2025년 1월 14일(화) 오후 3시

🔸발표자 : 황윤태 (University of Oxford Postdoctoral Researcher)

🔸강연주제: Geodesic flow kernels for semi-supervised learning on mixed variable tabular dataset

– This seminar will be conducted in Korean

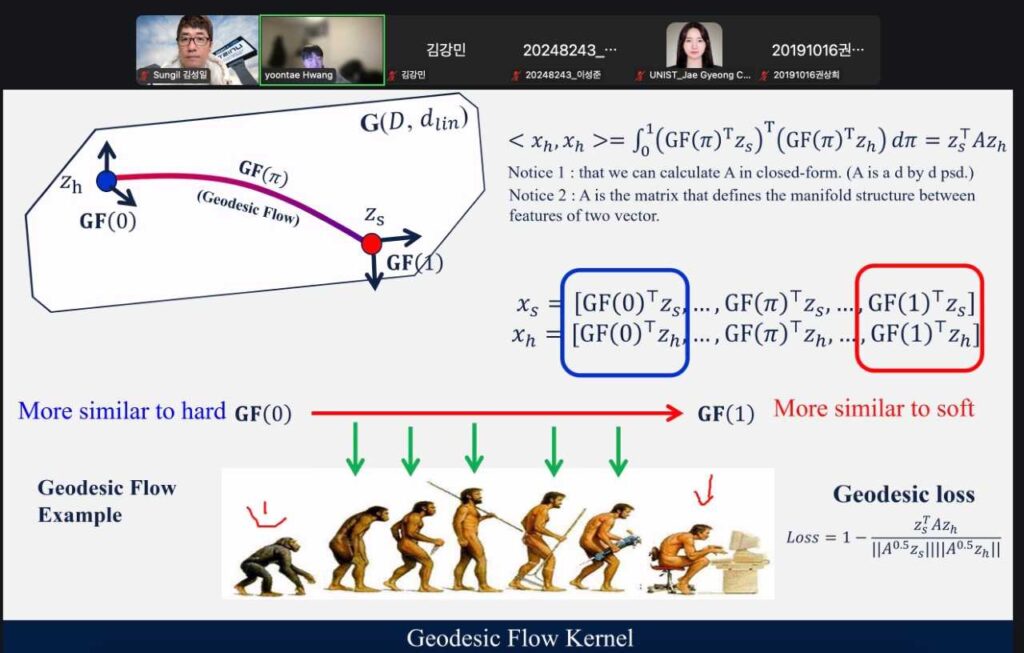

📑Abstract: Tabular data poses unique challenges due to its heterogeneous nature, combining both continuous and categorical variables. Existing approaches often struggle to effectively capture the underlying structure and relationships within such data. We propose GFTab (Geodesic Flow Kernels for Semi- Supervised Learning on Mixed-Variable Tabular Dataset), a semi-supervised framework specifically designed for tabular datasets. GFTab incorporates three key innovations: 1) Variable-specific corruption methods tailored to the distinct properties of continuous and categorical variables, 2) A Geodesic flow kernel based similarity measure to capture geometric changes between corrupted inputs, and 3) Tree-based embedding to leverage hierarchical relationships from available labeled data. To rigorously evaluate GFTab, we curate a comprehensive set of 21 tabular datasets spanning various domains, sizes, and variable compositions. Our experimental results show that GFTab outperforms existing ML/DL models across many of these datasets, particularly in settings with limited labeled data.

⚡연사정보: Yoontae Hwang received his Ph.D. in Industrial Engineering from Ulsan National Institute of Science and Technology (UNIST) in August 2024. His dissertation on “Financial Representation Learning” supervised by Prof. Yongjae Lee. During his doctoral studies, he authored six papers published in peer-reviewed finance journals and AI conferences. Currently, he is a Postdoctoral Researcher (Sejong Science Fellowship) at the University of Oxford, working in Prof. Stefan Zohren’s laboratory on the intersection of artificial intelligence and quantitative finance. His research focuses on financial time-series analysis, portfolio optimization, and machine learning applications in financial markets.